All Categories

Featured

Table of Contents

Which one you select depends upon your needs and whether the insurance firm will authorize it. Policies can additionally last until specified ages, which in many cases are 65. As a result of the numerous terms it uses, level life insurance supplies prospective insurance holders with adaptable options. Beyond this surface-level info, having a higher understanding of what these strategies require will certainly aid guarantee you acquire a policy that satisfies your demands.

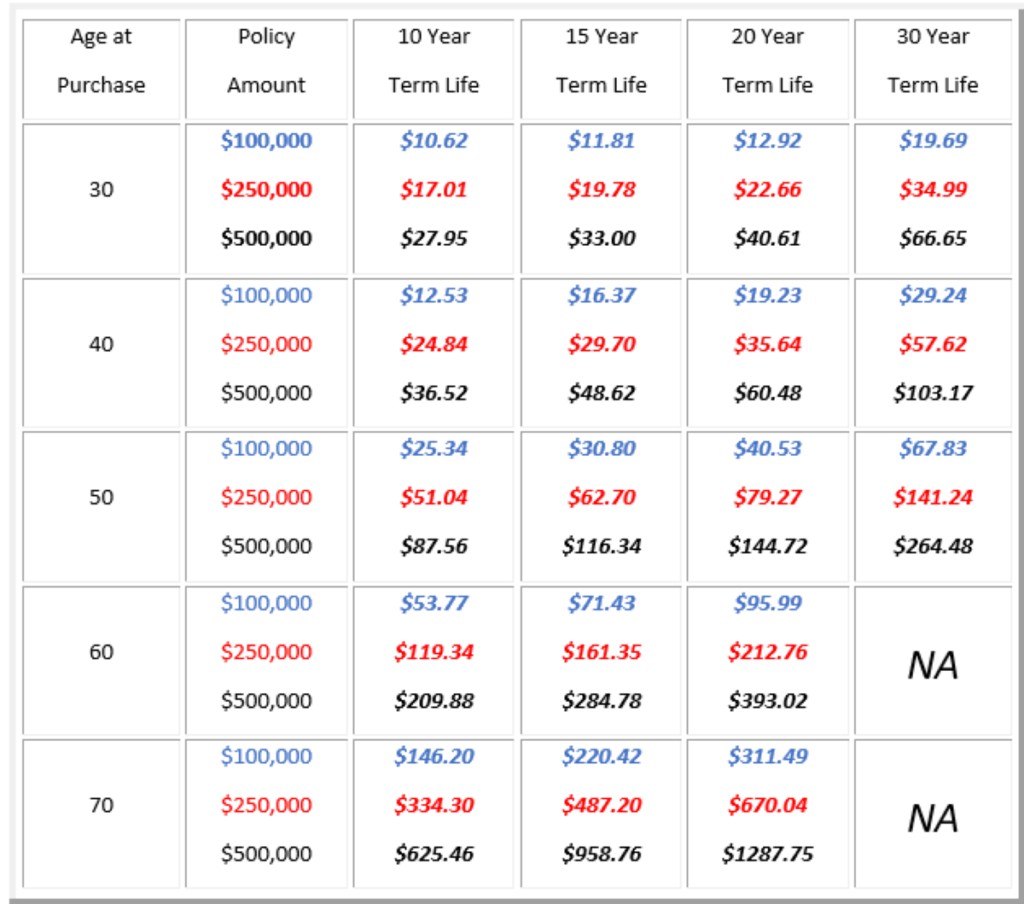

Be conscious that the term you select will certainly affect the costs you pay for the plan. A 10-year level term life insurance policy will certainly set you back much less than a 30-year policy due to the fact that there's much less opportunity of an event while the plan is active. Reduced danger for the insurer corresponds to reduce premiums for the insurance policy holder.

Your family's age need to additionally influence your plan term selection. If you have children, a longer term makes good sense due to the fact that it secures them for a longer time. If your youngsters are near the adult years and will be financially independent in the near future, a much shorter term might be a much better fit for you than a lengthy one.

When contrasting entire life insurance policy vs. term life insurance coverage, it deserves noting that the last typically sets you back much less than the previous. The result is much more insurance coverage with reduced premiums, providing the ideal of both worlds if you need a substantial amount of protection but can not pay for a more expensive plan.

What is Joint Term Life Insurance and How Does It Work?

A level survivor benefit for a term plan normally pays out as a round figure. When that takes place, your beneficiaries will certainly receive the entire quantity in a solitary settlement, which quantity is ruled out earnings by the internal revenue service. Those life insurance proceeds aren't taxable. Some degree term life insurance policy companies enable fixed-period payments.

Interest payments received from life insurance policy policies are considered income and undergo taxation. When your degree term life plan runs out, a couple of various points can occur. Some coverage terminates promptly with no option for renewal. In other scenarios, you can pay to prolong the strategy past its initial date or convert it right into a long-term plan.

The downside is that your eco-friendly level term life insurance will certainly come with greater premiums after its preliminary expiration. Advertisements by Cash.

Life insurance policy companies have a formula for computing danger using mortality and interest (What is level term life insurance). Insurance providers have countless customers securing term life policies simultaneously and utilize the costs from its energetic plans to pay enduring recipients of various other policies. These firms make use of death tables to approximate exactly how numerous people within a specific team will submit death claims each year, which information is used to determine typical life span for possible policyholders

Additionally, insurance policy firms can invest the cash they get from costs and enhance their income. The insurance policy business can invest the money and earn returns.

The following section details the advantages and disadvantages of level term life insurance coverage. Predictable premiums and life insurance policy protection Streamlined policy framework Potential for conversion to long-term life insurance policy Limited insurance coverage duration No cash money value build-up Life insurance policy premiums can boost after the term You'll find clear advantages when contrasting degree term life insurance to other insurance types.

What is Term Life Insurance For Spouse? Understanding Its Purpose?

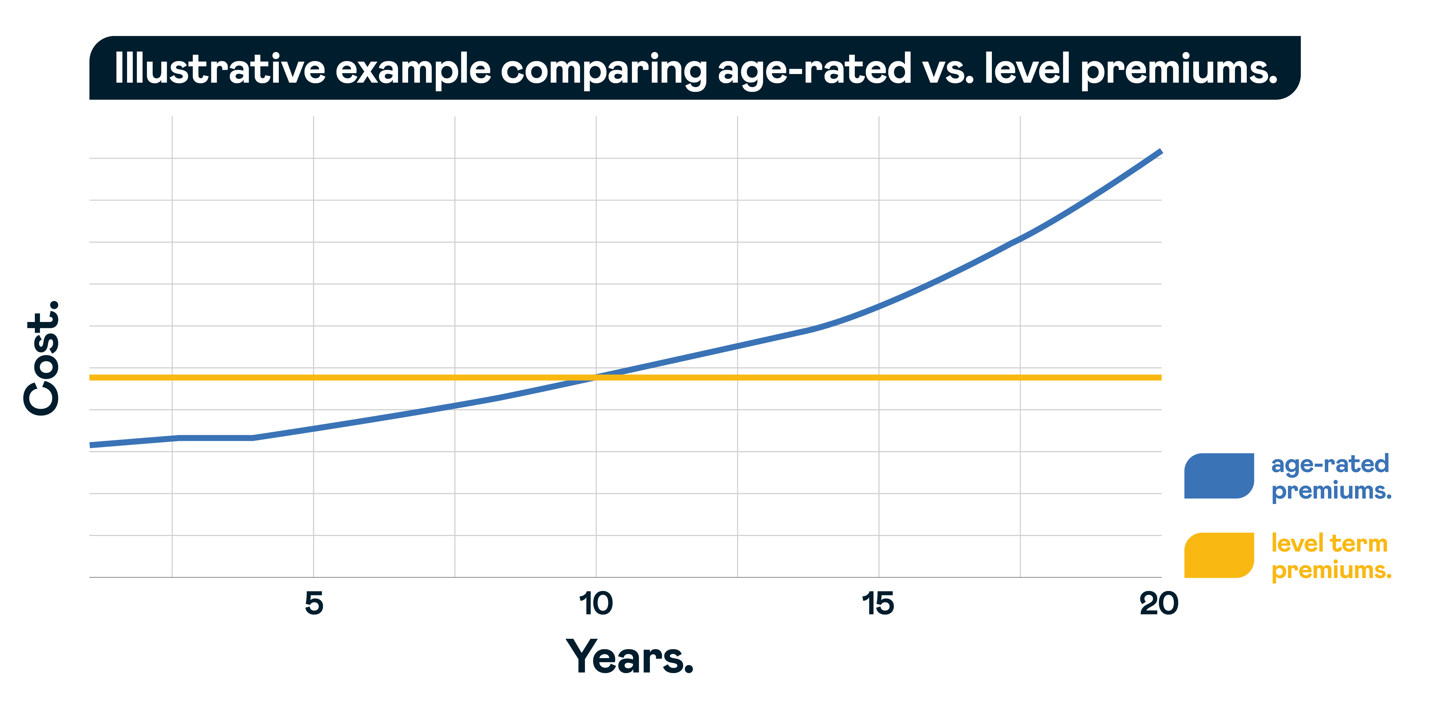

You constantly recognize what to anticipate with low-cost degree term life insurance protection. From the minute you secure a policy, your premiums will never alter, assisting you prepare monetarily. Your coverage won't differ either, making these plans reliable for estate planning. If you value predictability of your settlements and the payments your beneficiaries will receive, this sort of insurance policy might be a great fit for you.

If you go this course, your costs will certainly boost however it's always excellent to have some versatility if you wish to keep an active life insurance policy. Renewable degree term life insurance policy is an additional choice worth thinking about. These policies permit you to maintain your current strategy after expiry, providing flexibility in the future.

What is Increasing Term Life Insurance? Comprehensive Guide

Unlike a entire life insurance policy plan, degree term protection does not last indefinitely. You'll select a coverage term with the very best level term life insurance policy prices, but you'll no much longer have insurance coverage once the plan expires. This downside might leave you clambering to find a brand-new life insurance policy in your later years, or paying a premium to prolong your existing one.

Numerous entire, universal and variable life insurance policy plans have a money worth element. With among those plans, the insurance firm deposits a part of your month-to-month premium settlements into a cash worth account. This account earns rate of interest or is invested, helping it grow and provide a much more significant payment for your recipients.

With a level term life insurance policy policy, this is not the instance as there is no money value component. Consequently, your plan won't grow, and your survivor benefit will certainly never ever boost, therefore limiting the payment your recipients will get. If you want a policy that offers a death benefit and builds cash money value, consider entire, universal or variable strategies.

The second your policy ends, you'll no much longer have life insurance protection. Degree term and lowering life insurance coverage deal similar plans, with the major distinction being the fatality advantage.

Life insurance isn’t just a policy; it’s a powerful way to secure your family’s financial stability. From protecting your loved ones from unexpected costs to planning for the future, the right life insurance policy ensures peace of mind. Term life insurance is a popular choice for those seeking temporary, cost-effective coverage, while whole life insurance provides lifelong protection and cash value growth. Universal life insurance is another flexible option, ideal for families and individuals looking to balance affordability with long-term financial goals.

For specific needs, final expense insurance ensures funeral costs are covered, and mortgage protection life insurance provides reassurance that your family can stay in their home. Accidental death insurance adds another layer of security for unique situations. Many of these policies also include living benefits, allowing policyholders to access funds during critical times, such as illness or emergencies.

Life insurance isn’t just about protecting your loved ones; it’s also a strategic tool for building a solid financial foundation. business key person insurance agents. Speak with a licensed insurance agent today to explore policies designed for your specific needs, whether you’re planning for retirement, saving for college, or securing your family’s future. Request a free quote now to start building a secure tomorrow

It's a kind of cover you have for a specific quantity of time, understood as term life insurance policy. If you were to die while you're covered for (the term), your loved ones get a set payout concurred when you get the policy. You simply pick the term and the cover quantity which you can base, for instance, on the price of raising youngsters till they leave home and you could utilize the settlement towards: Helping to pay off your home mortgage, debts, charge card or financings Assisting to spend for your funeral prices Assisting to pay college fees or wedding prices for your kids Helping to pay living expenses, replacing your revenue.

How Does 30-year Level Term Life Insurance Policy Work?

The policy has no cash worth so if your repayments quit, so does your cover. The payout continues to be the same throughout the term. As an example, if you take out a degree term life insurance policy you can: Choose a fixed quantity of 250,000 over a 25-year term. If during this moment you die, the payment of 250,000 will be made.

{kind=link}

Table of Contents

Latest Posts

Insurance To Cover Funeral Costs

Final Cost Life Insurance

Final Expense Carriers

More

Latest Posts

Insurance To Cover Funeral Costs

Final Cost Life Insurance

Final Expense Carriers