All Categories

Featured

Table of Contents

- – What is the Purpose of Increasing Term Life In...

- – What is Term Life Insurance With Accidental De...

- – What is Level Term Life Insurance Meaning? Un...

- – What is Term Life Insurance With Level Premiu...

- – What is Level Term Life Insurance Policy? De...

- – Why Direct Term Life Insurance Meaning Could...

If George is detected with a terminal disease during the initial policy term, he probably will not be qualified to restore the policy when it runs out. Some plans provide ensured re-insurability (without evidence of insurability), however such functions come with a higher cost. There are numerous sorts of term life insurance policy.

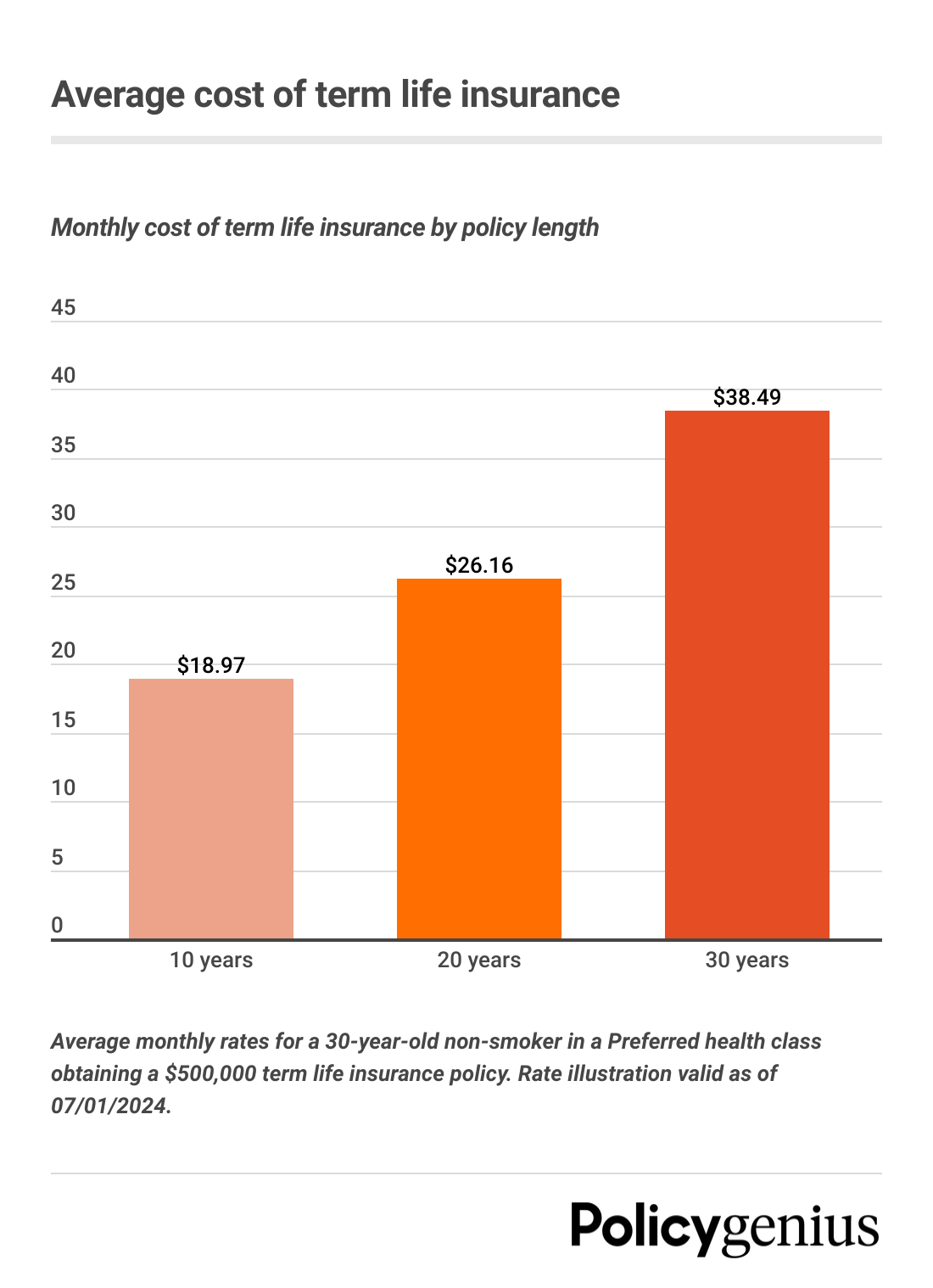

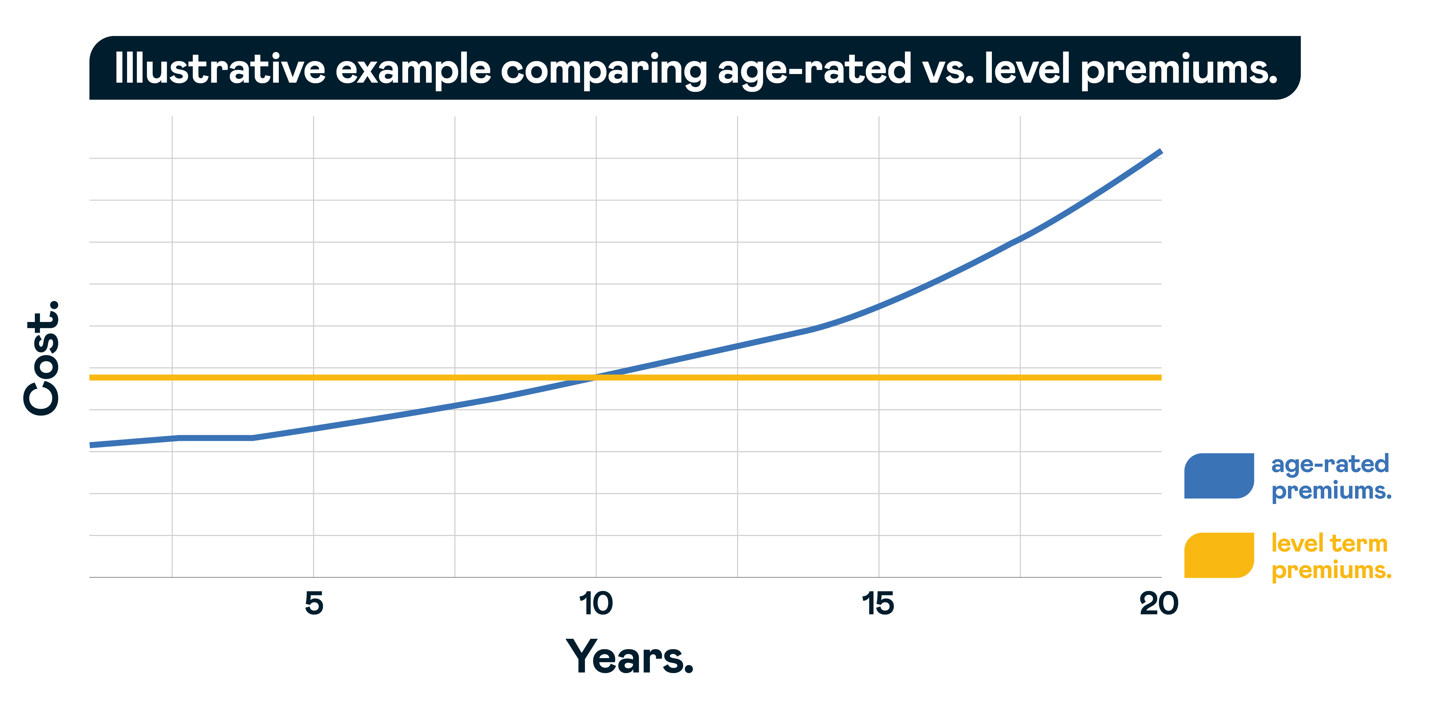

Usually, most business use terms varying from 10 to three decades, although a few offer 35- and 40-year terms. Level-premium insurance coverage has a fixed regular monthly settlement for the life of the plan. Most term life insurance has a level costs, and it's the type we have actually been referring to in many of this short article.

Term life insurance policy is appealing to youths with kids. Moms and dads can obtain significant coverage for a reduced cost, and if the insured passes away while the policy holds, the family members can count on the survivor benefit to replace lost earnings. These policies are additionally fit for people with growing family members.

What is the Purpose of Increasing Term Life Insurance?

Term life plans are perfect for individuals who desire considerable protection at a low price. Individuals who possess entire life insurance coverage pay extra in premiums for less coverage yet have the safety of knowing they are safeguarded for life.

The conversion rider must allow you to transform to any type of permanent plan the insurer provides without constraints. The primary features of the biker are preserving the original health score of the term plan upon conversion (also if you later on have wellness issues or become uninsurable) and making a decision when and just how much of the insurance coverage to transform.

Of training course, total costs will enhance substantially because entire life insurance policy is more costly than term life insurance coverage. Medical problems that create during the term life period can not cause premiums to be increased.

What is Term Life Insurance With Accidental Death Benefit and Why Choose It?

Entire life insurance coverage comes with substantially greater monthly premiums. It is implied to supply insurance coverage for as long as you live.

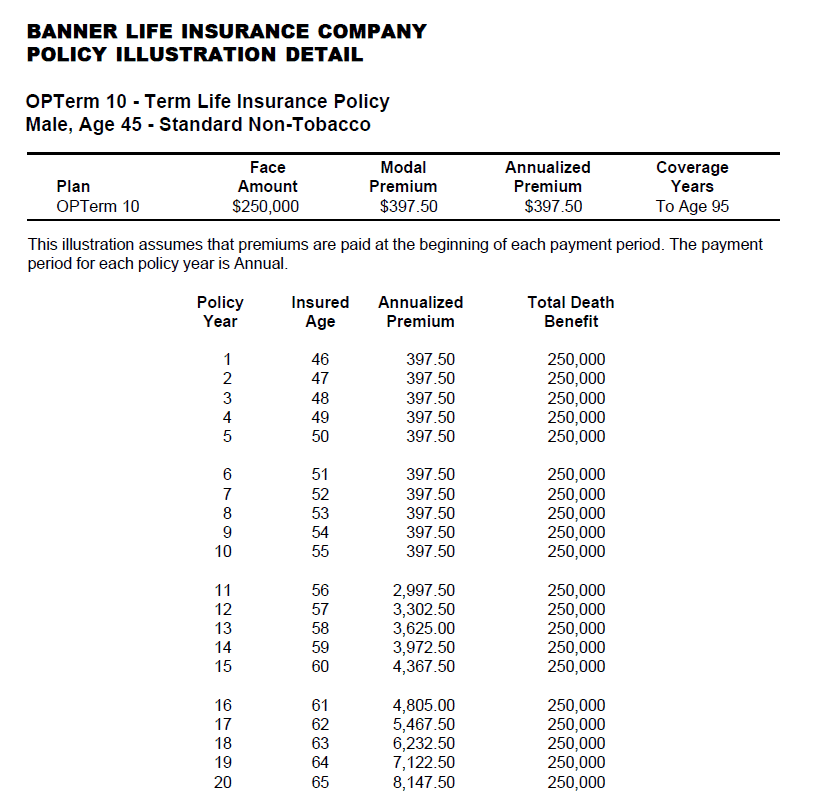

Insurance coverage firms established a maximum age restriction for term life insurance policies. The costs additionally increases with age, so a person aged 60 or 70 will pay substantially more than somebody years younger.

Term life is somewhat similar to vehicle insurance. It's statistically not likely that you'll require it, and the premiums are cash down the tubes if you do not. If the worst takes place, your family will obtain the benefits.

What is Level Term Life Insurance Meaning? Understand the Details

Essentially, there are two sorts of life insurance policy strategies - either term or permanent plans or some combination of the two. Life insurance providers provide different types of term strategies and standard life plans in addition to "passion delicate" items which have actually become a lot more widespread since the 1980's.

Term insurance coverage supplies defense for a specific period of time. This duration can be as brief as one year or provide protection for a specific number of years such as 5, 10, twenty years or to a defined age such as 80 or sometimes as much as the earliest age in the life insurance policy mortality tables.

What is Term Life Insurance With Level Premiums? Pros, Cons, and Considerations?

Presently term insurance policy prices are extremely competitive and amongst the most affordable traditionally experienced. It needs to be noted that it is a widely held idea that term insurance coverage is the least expensive pure life insurance policy protection available. One needs to review the plan terms very carefully to make a decision which term life choices appropriate to meet your specific situations.

With each brand-new term the premium is increased. The right to renew the policy without proof of insurability is an important advantage to you. Or else, the threat you take is that your wellness may wear away and you may be not able to obtain a policy at the exact same rates or even in all, leaving you and your beneficiaries without protection.

nfinite banking is a financial strategy that empowers you to take control of your finances using the cash value of a whole life insurance policy. By becoming your own banker, you can leverage the cash value to fund large expenses, invest in business opportunities, or handle emergencies—all while your money continues to grow tax-free. For business owners, infinite banking is an invaluable tool for maintaining financial independence and flexibility.

Whole life insurance policies designed for infinite banking offer stability and predictability, ensuring steady cash value growth over time. final expense life insurance brokers. Policies with living benefits further enhance their appeal, offering access to funds for critical illnesses or other urgent needs. Whether you’re looking to finance major purchases, grow your business, or achieve financial independence, infinite banking adapts to your goals while providing long-term security

This concept is especially beneficial for individuals and families seeking flexible financial solutions or business owners aiming to optimize their cash flow. Learn more about how infinite banking can transform your financial future. Schedule a free consultation today and take the first step toward achieving complete financial control.

You need to exercise this option during the conversion period. The length of the conversion period will certainly differ depending upon the kind of term policy purchased. If you convert within the proposed period, you are not needed to provide any kind of details concerning your wellness. The premium rate you pay on conversion is generally based on your "existing acquired age", which is your age on the conversion date.

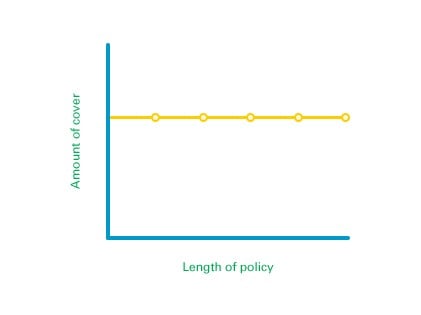

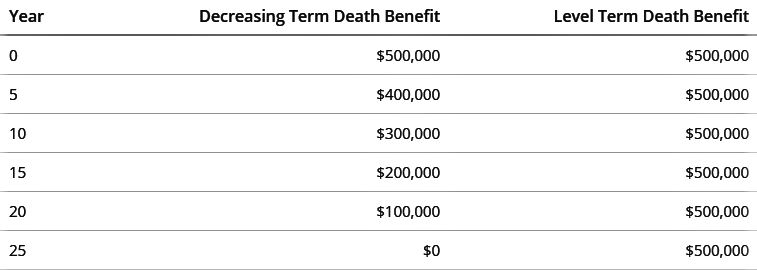

Under a level term plan the face quantity of the policy remains the same for the whole duration. With reducing term the face quantity minimizes over the duration. The premium remains the exact same annually. Typically such policies are marketed as home mortgage defense with the quantity of insurance coverage decreasing as the balance of the home mortgage reduces.

Typically, insurance firms have actually not had the right to transform premiums after the plan is offered. Given that such plans may continue for several years, insurers have to use conventional death, rate of interest and expense rate quotes in the premium computation. Flexible costs insurance coverage, nonetheless, permits insurance firms to supply insurance policy at reduced "current" costs based upon less conservative presumptions with the right to alter these premiums in the future.

What is Level Term Life Insurance Policy? Detailed Insights?

While term insurance coverage is created to provide protection for a defined amount of time, irreversible insurance policy is designed to give insurance coverage for your whole life time. To keep the premium rate level, the premium at the younger ages exceeds the real price of security. This additional costs builds a book (cash money worth) which helps spend for the policy in later years as the cost of security increases over the premium.

Under some policies, costs are needed to be spent for an established variety of years (What does level term life insurance mean). Under other policies, costs are paid throughout the insurance policy holder's life time. The insurance firm spends the excess premium bucks This sort of plan, which is often called cash worth life insurance, generates a financial savings component. Cash money worths are vital to a long-term life insurance policy.

Often, there is no relationship between the size of the money value and the premiums paid. It is the money worth of the policy that can be accessed while the insurance policy holder is alive. The Commissioners 1980 Criterion Ordinary Mortality Table (CSO) is the present table utilized in calculating minimum nonforfeiture values and policy books for common life insurance policy policies.

Why Direct Term Life Insurance Meaning Could Be the Best Option?

Several irreversible policies will contain provisions, which specify these tax obligation requirements. There are two standard categories of long-term insurance policy, traditional and interest-sensitive, each with a variety of variations. On top of that, each category is generally available in either fixed-dollar or variable type. Standard whole life policies are based upon long-lasting price quotes of expenditure, rate of interest and death.

{kind=link}

Table of Contents

- – What is the Purpose of Increasing Term Life In...

- – What is Term Life Insurance With Accidental De...

- – What is Level Term Life Insurance Meaning? Un...

- – What is Term Life Insurance With Level Premiu...

- – What is Level Term Life Insurance Policy? De...

- – Why Direct Term Life Insurance Meaning Could...

Latest Posts

Insurance To Cover Funeral Costs

Final Cost Life Insurance

Final Expense Carriers

More

Latest Posts

Insurance To Cover Funeral Costs

Final Cost Life Insurance

Final Expense Carriers